Balancing The Ledger Account JSS3 Business Studies Lesson Note

Download Lesson NoteTopic: Balancing The Ledger Account

A ledger is a principal book in which transactions are recorded in a summarized form. It is the final destination of all transactions in the subsidiary book.

Format of ledger Dr Cr

| Date | Particular | Folio | Amount | Date | Particular | Folio | Amount |

| N | N |

SIMPLE CLASSIFICATION OF LEDGER ACCOUNT

- PERSONAL ACCOUNT: This ledger account records the person account such as debtors, creditors, capital, and bank account

- IMPERSONAL ACCOUNT: This records non–person accounts such as real and nominal accounts.

- Real Account: records the assets of the business such as building, motor vehicle, furniture, stock, etc.

- Nominal Account: records the income and expenses of the business such as insurance, transport, salary, etc.

Ledger Account is divided into

- Sales ledger/debtors ledger

- Purchases ledger/creditors ledger

- General ledger

- Private ledger

SALES LEDGER/DEBTORS LEDGER: This is used to record accounts relating to debtors. Debtors are those who owe money that belongs to an organisation.

PURCHASES LEDGER: This records the account of creditors. Creditors are people to whom money is owned or persons from whom goods have been bought.

GENERAL LEDGER: This takes care of both real and nominal account

PRIVATE LEDGER: This is a ledger where properties’ confidential accounts are recorded.

Items in a ledger:

There are two sides to the ledger- the debit side and the credit side. The items below are found on both sides of the ledger.

- Date: The date and month the transaction took place.

- Particulars: The column which shows the detail of the transaction that took place.

- Folio: The page number of the subsidiary book where the transaction was transferred from

- Amount: This is the amount of money received or spent.

- Discount: This is the column where the discount allowed or the discount received is recorded.

.

How to record cash received and payment

Step 1.

Recording a transaction in a journal marks the starting point for the double-entry bookkeeping system. In this system, the financial structure of an organization is analyzed as consisting of many interrelated aspects, each of which is called an account (for example, the “wages payable” account). Every transaction is identified by its two or more aspects or dimensions, referred to as its debit (or left side) and credit (or right side) aspects and each of these aspects has an effect on the financial structure.

Depending on their nature, certain accounts are increased with debits and decreased with credits; other accounts are increased with credits and decreased with debits. For example, the purchase of merchandise for cash increases the merchandise account (a debit) and decreases the cash account (a credit). If merchandise is purchased based on a promise to make a future payment, a liability would be created, and the journal entry would record an increase in the merchandise asset account (a debit) and an increase in a liability account (a credit). Recognition of wages earned by employees entails recording an increase in the wage-expense account (a debit) and an increase in a liability account (a credit). The subsequent payment of the wages would be a decrease in the cash asset account (a credit) and a decrease in the liability account (a debit).

Step 2

In addition to the general ledger, a subsidiary ledger is used to provide information in greater detail about the accounts in the general ledger. For example, the general ledger contains one account showing the entire amount owed to the enterprise by all its customers; the subsidiary ledger breaks this amount down on a customer-by-customer basis, with a separate subsidiary account for each customer. Subsidiary accounts may also be kept for the wages paid to each employee, for each building or machine owned by the company, and for amounts owed to each of the enterprise’s creditors.

Step 3

Posting data to the ledgers is followed by listing the balances of all the accounts and calculating whether the sum of all the debit balances agrees with the sum of all the credit balances (because every transaction has been listed once as a debit and once as a credit). This determination is called a trial balance. This procedure and those that follow it take place at the end of the fiscal period. Once the trial balance has been prepared successfully, the bookkeeping portion of the accounting cycle has ended.

Step 4

Once bookkeeping procedures have been completed, the accountant prepares adjustments to recognize events that, although they did not occur in conventional form, are in substance already completed transactions. The following are the most common circumstances that require adjustments: accrued revenue (for example, interest earned but not yet received); accrued expense (wage cost incurred but not yet paid); unearned revenue (earning subscription revenue that had been collected in advance); prepaid expense (expiration of a prepaid insurance premium); depreciation (recognizing the cost of a machine as expense spread over its useful economic life); inventory (recording the cost of goods sold based on a period’s purchases and the change between beginning and ending inventory balances); and receivables (recognizing bad-debt expenses based on expected uncollected amounts).

Steps 5 and 6

Once the adjustments are calculated and entered in the ledger, the accountant prepares an adjusted trial balance—one that combines the original trial balance with the effects of the adjustments (step five). With the balances in all the accounts thus updated, financial statements are then prepared (step six). The balances in the accounts are the data that make up the organization’s financial statements.

Step 7

The final step is to close noncumulative accounts. This procedure involves a series of bookkeeping debits and credits to transfer sums from income-statement accounts into owners’ equity accounts. Such transfers reduce to zero the balances of noncumulative accounts so that these accounts can receive new debit and credit amounts that relate to the activity of the next business period.

The rule: – debit cash received in the cash book and credit cash paid in the cash book.

CONTRA ENTRIES

This occurs when the debit and credit entries are made in the same account.

EVALUATION

- What is a ledger?

- Define contra entry.

READING ASSIGNMENT

Business Studies for JSS2 by O.A Lawal et al pg58-60.

GENERAL EVALUATION

- What is a market?

- Who is the receptionist?

- Mention four documents handled by a receptionist.

- What is a mail?

- What is an office document?

Weekend assignment

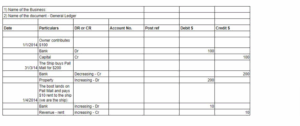

Post the following in a ledger

- 5/1/09 (a) Mr. Ojo started a business with N10,000

- 10/1/09 (b) bought office equipment by cash N3000

- 15/1/09 © bought goods in cash N3000

- 20/1/09 (d) paid wages in cash N12000

- 28/1/09 (e) received commission by cash N4000

THEORY

- Write a short note on the ledger

- What are the steps in preparing a ledger?

Second Term Business Studies Lesson Notes for Other Topics

Need For Monitoring And Control Of Chemicals

Explore lesson notes covering all topics.

Consumer, Market, And Society

Explore lesson notes covering all topics.

Factors Of Production

Explore lesson notes covering all topics.

Types Of Occupation

Explore lesson notes covering all topics.

Honesty In Business

Explore lesson notes covering all topics.

Ethics In Sourcing Chemicals

Explore lesson notes covering all topics.

Entrepreneurship

Explore lesson notes covering all topics.

Importance Of Entrepreneurship

Explore lesson notes covering all topics.

Forms Of Business Organization

Explore lesson notes covering all topics.

Bookkeeping Ethics

Explore lesson notes covering all topics.

How To Make Complaints

Explore lesson notes covering all topics.

Personal Finance

Explore lesson notes covering all topics.

Trial Balance

Explore lesson notes covering all topics.

Trading Profit And Loss Account

Explore lesson notes covering all topics.

Balance Sheet

Explore lesson notes covering all topics.

Lesson Notes for Other Classes

Basic 2 Lesson Note

The complete lesson note to guide your studies.

Basic 3 Lesson Note

The complete lesson note to guide your studies.

Basic 4 Lesson Note

The complete lesson note to guide your studies.

Basic 5 Lesson Note

The complete lesson note to guide your studies.

JSS1 Lesson Note

The complete lesson note to guide your studies.

JSS2 Lesson Note

The complete lesson note to guide your studies.