Principles Of Double Entry SS1 Book Keeping Lesson Note

Download Lesson NoteTopic: Principles Of Double Entry

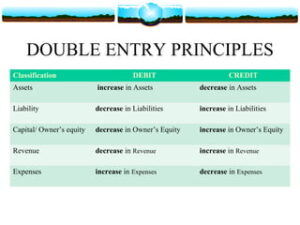

The principle states that for every debit entry, there must be a corresponding credit entry and

vice versa. It is the foundation of bookkeeping. The principle operates on the basis that every financial transaction must have two aspects i.e.:

Debit: Receiver’s account

Credit: Giver‘s account

Double entry is the act of recording business transactions twice in the books of account.

BENEFITS OF DOUBLE ENTRY

- It provides complete records of business transactions.

- It reduces the risk of fraud and facilitates the correction of errors.

- It provides a basis for the test of arithmetical accuracy of the accounting records.

- It is a means of providing financial information that may be the product of the accounting process.

- Double entry aids the effective implementation and review of the internal control system of any organization.

ILLUSTRATION ON THE PRINCIPLE OF DOUBLE ENTRY

- Jan 1 Mr Chidera started the business with N10,000

Effect

Increase in capital: Capital account

Increase in asset: Cash account

Action required: Dr Cash account-Receiver

Cr Capital account -Giver

- Jan 2 Paid N450 cash for rent

Effect

Increase in expenditure: Rent account

Decrease in asset: Cash account

Action required: Dr Rent account-Receiver

Cr Cash account-Giver

- Jan 3 bought office equipment N600, 000 by cheque

Effect

Increase in asset: Office Equipment account

Decrease in asset: Bank account

Action required: Dr Office Equipment account-Receiver

Cr Bank account-Giver

- Jan 8 Withdrew cheque for private use N2000

Effect

Increase in Drawings: Drawings account

Decrease in asset: Bank account

Action required: Dr Drawings account-Receiver

Cr Bank account-Giver

- Jan 9 Withdrew N600 cash from the bank for office use

Effect

Increase in asset: Cash account

Decrease in asset: Bank account

Action required: Dr Cash account-Receiver

Cr Bank account-Giver

- Jan 10 Received loan of N20,000 cash from Chinaza

Effect

Increase in asset: Cash account

Increase in liability: Loan account

Action required: Dr Cash account-Receiver

Cr loan account-Giver

Second Term Book Keeping Lesson Notes for Other Topics

Joint Venture Account

Explore lesson notes covering all topics.

Contract Account

Explore lesson notes covering all topics.

Introduction of Company Account

Explore lesson notes covering all topics.

Partnership Account II

Explore lesson notes covering all topics.

Partnership Account I

Explore lesson notes covering all topics.

Manufacturing Account

Explore lesson notes covering all topics.

Relational Models

Explore lesson notes covering all topics.

Entreprenuership Education

Explore lesson notes covering all topics.

Control Account

Explore lesson notes covering all topics.

Stock Evalaution

Explore lesson notes covering all topics.

Bad Debts And Doubtful Debts

Explore lesson notes covering all topics.

Ledgers

Explore lesson notes covering all topics.

Books Of Original Entry

Explore lesson notes covering all topics.

Single Column Cash Book

Explore lesson notes covering all topics.

Double Column Cash Book

Explore lesson notes covering all topics.

Lesson Notes for Other Classes

JSS1 Lesson Note

The complete lesson note to guide your studies.

JSS2 Lesson Note

The complete lesson note to guide your studies.

SS2 Lesson Note

The complete lesson note to guide your studies.

SS3 Lesson Note

The complete lesson note to guide your studies.