Cost Concept SS2 Economics Lesson Note

Download Lesson NoteTopic: Cost Concept

MEANING OF COST OF PRODUCTION

Cost of production can be defined as the sum of the total of all the payments to the factors of production used in the production of goods and services.

For goods and services to be produced, all the four factors of production, which are land, capital, labour and entrepreneur, must work together.

ECONOMIST’S VIEW OF COST

Economists view cost as opportunity cost. He is not concerned about the real amount of money spent on a particular item but the value of the sacrificed alternative. For example, if an individual bought a shoe instead of a handset. The opportunity cost is the handset forgone.

ACCOUNTANT’S VIEW OF COST

To an accountant, cost is the total amount of money spent to acquire a product.

TYPES OF COST

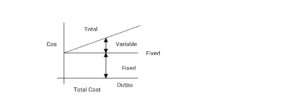

- Total Cost (TC): Total cost may be defined as the total sum of fixed and variable costs incurred by an enterprise in the production of a particular commodity.

Total cost = Fixed cost + variable cost or Average cost x Quantity.

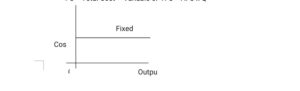

- Fixed Cost (FC): Fixed cost, also called overhead cost or unavoidable cost, is defined as the cost that remains constant in the short run no matter the level of output. E.g. money spent on rent, etc.

FC = Total Cost – Variable or TFC = AFC x Q

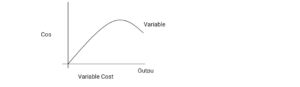

- Variable Cost (COST): Variable cost, also called direct cost, is defined as the cost of production which varies or changes directly with the level of output. E.g. cost of raw materials, labour, etc. VC = TC – FC

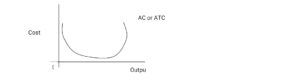

4. Average Cost (AC) OR Average Total Cost (ATC): Average cost is defined as cost per unit of output.

Average cost is the total cost of producing a given output divided by the number of units of output.

AC = Total cost ÷ Total Output OR

ATC = AFC + AVC

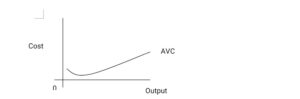

- Average Variable Cost: The average variable cost is the cost per unit of variable cost of output.

AVC = TVC ÷ TQ = ATC – AFC

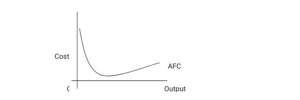

- Average Fixed Cost (AFC): This is the fixed cost per unit of output.

AFC = Total fixed cost

Quantity

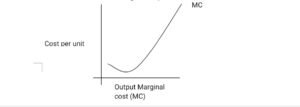

- Marginal Cost (MC): It is referred to as incremental cost. Marginal cost is the addition to the total cost needed to produce a unit increase in output.

Marginal cost does not depend on fixed cost but on variable cost, because fixed cost does not vary with the level of output.

Marginal Cost = Change in TC

Change in output

Second Term Economics Lesson Notes for Other Topics

Economic Growth and Development

Explore lesson notes covering all topics.

Balance of Payments (B.O.P) 2

Explore lesson notes covering all topics.

Balance of Payments (B.O.P) 1

Explore lesson notes covering all topics.

Economic Reform Programmes

Explore lesson notes covering all topics.

Economic Development Challenges

Explore lesson notes covering all topics.

Current Economic Plans MDGs NEEDS Vision 2030

Explore lesson notes covering all topics.

International Economic Organization

Explore lesson notes covering all topics.

Economic Development Planning

Explore lesson notes covering all topics.

Imperfect Market

Explore lesson notes covering all topics.

Industries In Nigeria

Explore lesson notes covering all topics.

Market Structure

Explore lesson notes covering all topics.

Supply And Demand Of Labour

Explore lesson notes covering all topics.

Labour Market

Explore lesson notes covering all topics.

Economics System

Explore lesson notes covering all topics.

Production Possibility Curve

Explore lesson notes covering all topics.

Lesson Notes for Other Classes

JSS1 Lesson Note

The complete lesson note to guide your studies.

JSS2 Lesson Note

The complete lesson note to guide your studies.

SS1 Lesson Note

The complete lesson note to guide your studies.

SS3 Lesson Note

The complete lesson note to guide your studies.