Income And Expenditure Account SS2 Book Keeping Lesson Note

Download Lesson NoteTopic: Income And Expenditure Account

The income and Expenditure Account is a nominal account prepared by not-for-profit organizations to ascertain the surplus or deficit of the organization for the current accounting year. It is prepared at the end of the accounting year by debiting all the expenses and losses and crediting all incomes and gains of the concerned year in this account to ascertain the result of either surplus or deficit. The Income and Expenditure Account is prepared on an accrual basis of accounting and records income and expenses of a revenue nature only.

The Income and Expenditure Account is similar to the Profit & Loss Account of a business organization, which ascertains the profit or loss of the business for the concerned year. Profit and Loss a/c ascertain profit or loss and since Not-for-Profit-organization is established for the welfare and service motive of the society, it prepares an Income and Expenditure Account to know the surplus or deficit of the organization.

The surplus or deficit ascertained from the Income and Expenditure Account is transferred to the Capital Fund in the Balance Sheet. The difference between the two sides is either surplus( if the total of the Income side is more than the Expenditure side) or deficit( the Expenditure side is more than the Surplus side), which is added or deducted from the Capital Fund in Balance Sheet, as the case may be. The income and Expenditure Account records the non-cash expenditure, such as depreciation.

Income and Expenditure Account is prepared from trial balance when complete sets of books are maintained or from Receipt & Payment a/c when complete sets of books are not maintained by the organizations.

FEATURES OF INCOME AND EXPENDITURE ACCOUNT

- Revenue Nature: The income and Expenditure Account is a nominal

account which records transactions and events of a revenue nature. All the expenses and losses are debited and all incomes and gains are credited to this account.

- Accrual Basis of Recording: Income and Expenditure Account records transactions and events on an accrual basis of accounting.

- Current Period: The Income and Expenditure Account records only current periods’ incomes, expenses and losses whether paid or not. Revenue items relating to the preceding or succeeding period are excluded while preparing this account.

- Opening and Closing Balances: Income and Expenditure Account

does not have any opening balance. The balance at the end of the account represents the surplus or deficit of the accounting year. The surplus or the deficit is transferred to the capital fund in the balance sheet.

- Adjustments: The income and Expenditure Account takes into account all the adjustments to ascertain the surplus or deficit of an accounting year. It records adjustments relating to prepaid or outstanding provisions for depreciation and doubtful debts.

STEPS IN PREPARATION OF INCOME AND EXPENDITURE ACCOUNTS

Step 1: All the revenue receipts are credited to the income side of Income & Expenditure A/c. Adjustments related to the accounting year are to be made where amounts relating to the preceding and succeeding year are excluded, and the amount relating to the current year yet not received are

included.

Step 2: All the revenue expenditures are debited to Income and Expenditure A/c with due adjustments from the additional information provided relating to the accounts for the amounts received in advance and those outstanding.

Step 3: Record all the non-cash expenditures and gains to determine the surplus/deficit of the current year, such as:

- Depreciation of fixed assets

- Provision for doubtful debts, if required

- Profit or loss on sale of fixed assets

Step 4: Carefully read and record the necessary items from the Receipt & Payment a/c, if the Income and Expenditure Account is being prepared from it.

Step 5: The opening and closing balance of cash is not recorded, as they are not income.

Step 6: Transactions and events of a capital nature are not taken in Income and Expenditure A/c. Capital Receipts and Capital Payments are shown in the Balance Sheet.

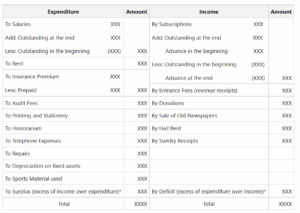

FORMAT OF INCOME AND EXPENDITURE ACCOUNT

- Name of the organization

- Income and Expenditure Account (for the year ended… )

* represents that the Income and Expenditure A/c will either have a Surplus or Deficit balance, i.e., when the income side is greater than the payment side, the difference is denoted as a Surplus, and when the payment side is more than the receipt side, the difference is denoted a Deficit.

EXAMPLES

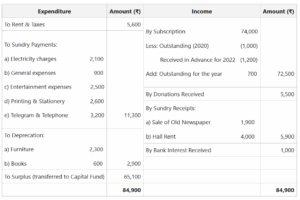

From the following information, prepare the Income and Expenditure Account of Geeks Foundation for the year ending 2021:

- Subscriptions received during the year ₹74,000, which included ₹1,000

for the year 2020 and ₹1,200 for the year 2022.

- Rent and Taxes paid during the year ₹5,600.

- Outstanding subscription for the year 2021 amounts to ₹700.

- Sundry payments include:

- Electricity charges ₹2,100

- General expenses ₹ 900

iii. Entertainment expenses ₹ 2,500

- Printing and Stationery ₹ 2,600

- Telegram and Telephone expenses ₹3,200

- Sundry receipts included:

- Sale of old newspaper ₹1,900

- Hall rent received ₹4,000.

- Donations received ₹5,500

- Write off ₹2,300 from furniture and ₹600 from books

- Bank interest received ₹1,000

Solution:

Geeks Foundation Income and Expenditure Account (for the year ended 31st March,2021

Third Term Book Keeping Lesson Notes for Other Topics

Basic Concepts Of Marketing

Explore lesson notes covering all topics.

Receipt And Payment Account

Explore lesson notes covering all topics.

Account Of Non-Profit Making Organizations

Explore lesson notes covering all topics.

Single Entry And Incomplete Records

Explore lesson notes covering all topics.

Three Column Cash Book

Explore lesson notes covering all topics.

Petty Cashbook

Explore lesson notes covering all topics.

Trial Balance

Explore lesson notes covering all topics.

Lesson Notes for Other Classes

JSS1 Lesson Note

The complete lesson note to guide your studies.

JSS2 Lesson Note

The complete lesson note to guide your studies.

SS1 Lesson Note

The complete lesson note to guide your studies.

SS3 Lesson Note

The complete lesson note to guide your studies.