Three Column Cash Book SS1 Financial Accounting Lesson Note

Download Lesson NoteTopic: Three Column Cash Book

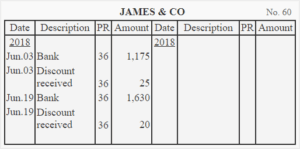

This type of Cash Book combines a discount column on both sides to the cash and bank column. The discounts allowed column is on the debit side, while the discounts received column is on the credit side. The principle of double entry is also applicable in the three-column Cash Book. It must be noted however that the discount allowed and the discount received columns though they have the appearance of account columns, are merely memoranda, from them, we can obtain periodic totals that will be entered into the discount accounts.

NOTE: The discount columns in the Cash Book are totaled and not balanced. They are to be added weekly or monthly at the time the cash and bank columns are balanced and ruled off. the totals of the discount columns are taken to the discount accounts in the ledger and are entered on the same sides of these accounts as they are found in the Cash Book

Second Term Financial Accounting Lesson Notes for Other Topics

Contract Account

Explore lesson notes covering all topics.

Hire Purchase Account

Explore lesson notes covering all topics.

Consignment Account

Explore lesson notes covering all topics.

Joint Venture Account

Explore lesson notes covering all topics.

Branch Account

Explore lesson notes covering all topics.

Preparation Of Personal Cost Budget

Explore lesson notes covering all topics.

Receipts And Payment Accounts

Explore lesson notes covering all topics.

Partnership Accounts II - Partnership Capital Accounts & How to Calculate it

Explore lesson notes covering all topics.

Partnership Accounts

Explore lesson notes covering all topics.

Single Entry And Incomplete Records

Explore lesson notes covering all topics.

Accounts Of Non Profit Making Organisations

Explore lesson notes covering all topics.

Trial Balance

Explore lesson notes covering all topics.

Accounting Concepts And Convention

Explore lesson notes covering all topics.

Final Account Of A Sole Trader

Explore lesson notes covering all topics.

Balance Sheet

Explore lesson notes covering all topics.

Lesson Notes for Other Classes

JSS1 Lesson Note

The complete lesson note to guide your studies.

JSS2 Lesson Note

The complete lesson note to guide your studies.

SS2 Lesson Note

The complete lesson note to guide your studies.

SS3 Lesson Note

The complete lesson note to guide your studies.